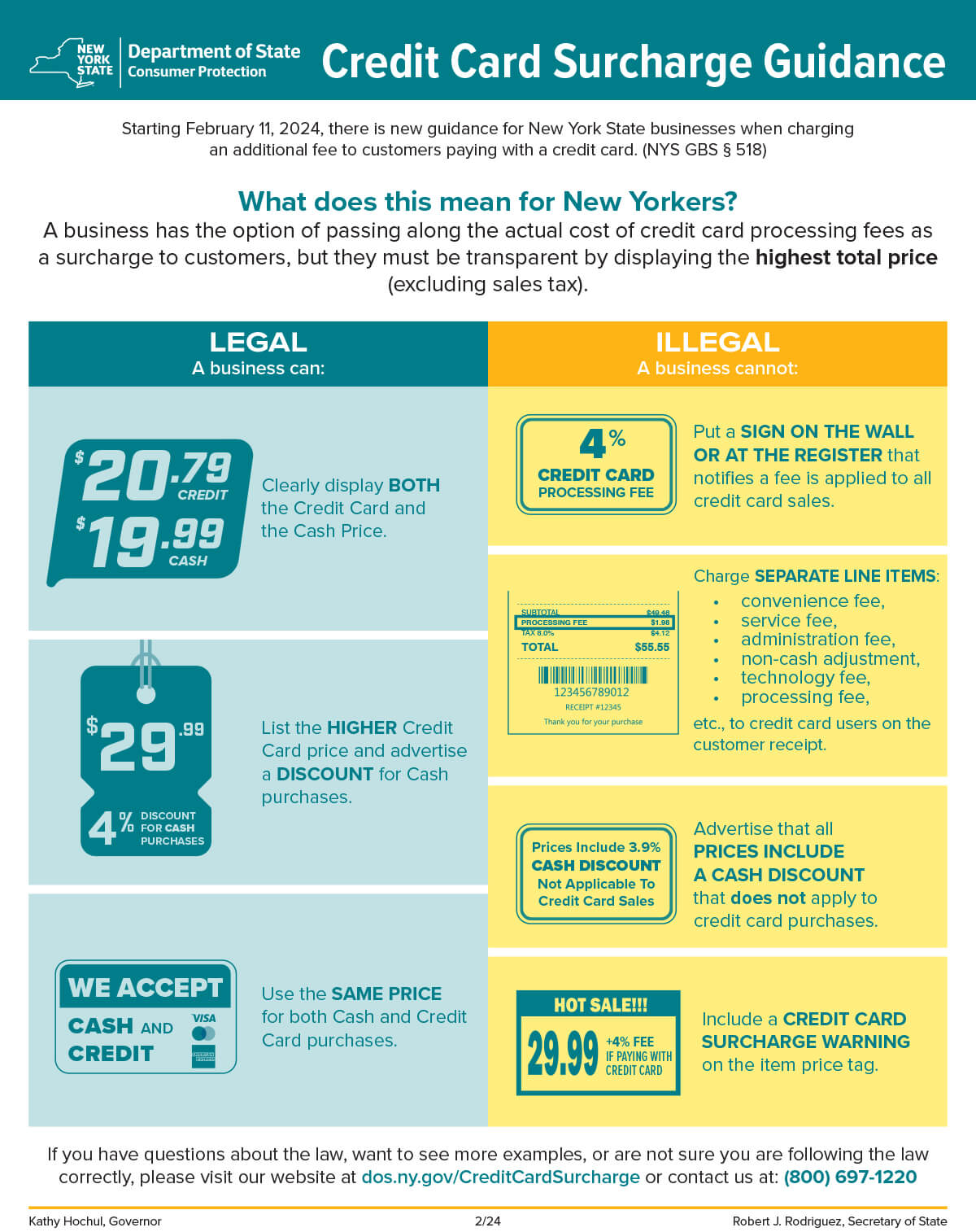

What’s Fueling Growing Conversation About the California Credit Card Surcharge?

A quiet but noticeable shift in financial awareness is underway across the U.S., particularly around how card issuers and merchants manage discretionary payment fees—now spotlighted by growing attention on the California Credit Card Surcharge. While not a new concept, rising consumer curiosity and digital transparency have placed it at the center of discussions about credit card usage, merchant policies, and financial flexibility. Game Conventions California This emerging topic reflects a broader trend: users increasingly seeking clarity about hidden costs and how policies impact their everyday spending.

Why the California Credit Card Surcharge Is Rising in Headlines

California’s recent move to cap surcharge fees on credit card transactions has become a focal point nationwide. Advocates highlight it as a consumer protection milestone, reducing merchant-driven fees that once added unexpected costs for cardholders. Meanwhile, business operators express concerns about administrative burden and market competitiveness. This dynamic has sparked debate across financial media, merchant networks, and wellness communities—driving user search intent and fueling demand for accurate, neutral explanations. Game Conventions California

How the California Credit Card Surcharge Actually Works

The California Credit Card Surcharge refers to employer-paid fees card networks charge merchants when customers use credit cards beyond the standard all-card limit. These fees historically allowed businesses to process surcharges, but California’s new regulations cap this payment, shifting costs back toward employers rather than cardholders. California Nevada Jatc Rather than imposing new fees directly on consumers, the law encourages transparency and limits hidden charges, helping users avoid surprise costs when paying with credit. Card issuers and merchants now operate under clearer disclosure rules, improving clarity in transaction processing.

Common Questions About the California Credit Card Surcharge

Q: Is the California Credit Card Surcharge now prohibited? Game Conventions California A: No, it’s not banned, but caps now limit employer-paid fees, reflecting a shift in how surcharge costs are managed and disclosed.

Q: Will I face unexpected surcharges when using my credit card? A: With California’s new rules, merchants must clearly disclose any fee shifts, minimizing unwarranted charges but requiring awareness of issuer policies. When Do Bass Spawn In California

Q: Who benefits most from this change? A: Consumers gain more predictable billing, while businesses face updated compliance requirements and potential cost adjustments.

Q: Does the surcharge affect all credit card transactions? A: Only transactions where limits are exceeded—credit users can anticipate transparency, not sudden fees.

Opportunities and Realistic Considerations

The California Credit Card Surcharge opens a path for improved financial clarity in a market where hidden costs often erode trust. For users, this means more predictable spending and clearer conversations with employers and card providers. For businesses, compliance demands careful policy alignment and communication. While not a universal solution, the policy supports informed choices—reducing friction, fostering transparency, and contributing to broader financial wellness efforts.

Myths That Commonly Confuse Readers

Myth: The surcharge now applies to all credit card use. Reality: It only applies when card limits are exceeded—most routine purchases remain unaffected.

Myth: Employers now fully absorb all credit card costs. Reality: The shift reallocates responsibility, requiring employers to absorb only approved fees under state oversight.

Myth: This policy eliminates credit card surcharging entirely. Reality: It caps and monitors surcharges rather than banning them outright.

Who Should Pay Attention to California’s Credit Card Surcharge Change?

The regulatory shift touches diverse groups across the U.S.: freelancers and small business owners monitoring operational costs, employees tracking payroll deductions, and consumers seeking clarity on credit card usage. It also affects entrepreneurs managing merchant payment systems, financial planners advising clients, and anyone interested in evolving consumer protection policies shaping digital finance.

A Gentle Call to Stay Informed and Engaged

The California Credit Card Surcharge reflects a quiet transformation in how fintech transparency meets everyday life. Rather than a sweeping innovation or sensational shift, it’s part of a growing movement toward clarity in financial friction points. By understanding how these fees work—and their bounds—you gain control over your spending, support fair employer practices, and contribute to more informed digital financial habits. Stay curious, stay informed, and keep engaging with the evolving tools that support a smarter, more transparent relationship with money.