California Mortgage Interest Deduction: Why It’s Rising in Public Conversation

Is the California Mortgage Interest Deduction quietly gaining momentum across the U.S.? For homeowners and prospective buyers navigating today’s complex home financing landscape, this tax benefit is increasingly relevant—especially as interest rates and housing costs remain high. When Are Watermelons In Season In California With federal and state tax policies evolving, more Californians are turning to this deduction to ease financial pressure, sparking growing interest across digital platforms and community discussions.

The rising attention centers on a key question: how does this longstanding tax advantage actually work, and can it truly help reduce homeownership costs in California’s tough market? Far from a simple write-off, the deduction offers a strategic way to offset mortgage interest expenses—but only for eligible homeowners. Understanding its mechanics, eligibility, and real-world impact can make a meaningful difference in household budgets.

Why California Mortgage Interest Deduction Is Gaining Traction Now

California’s tax environment, combined with national conversations around housing affordability, has amplified focus on the mortgage interest deduction. When Are Watermelons In Season In California Recent economic shifts—including higher interest rates and steady home price levels—have pushed many to reevaluate tax-efficient homeownership strategies. As discussions around tax policy and financial planning expand online, especially on mobile devices, both first-time buyers and seasoned investors are exploring how this deduction fits into their broader financial picture.

The data shows increasing digital engagement with messaging around tax relief, financial planning, and long-term investment—making California’s motor interest deduction a natural topic in search results seeking clarity and actionable insight.

How California’s Mortgage Interest Deduction Actually Works

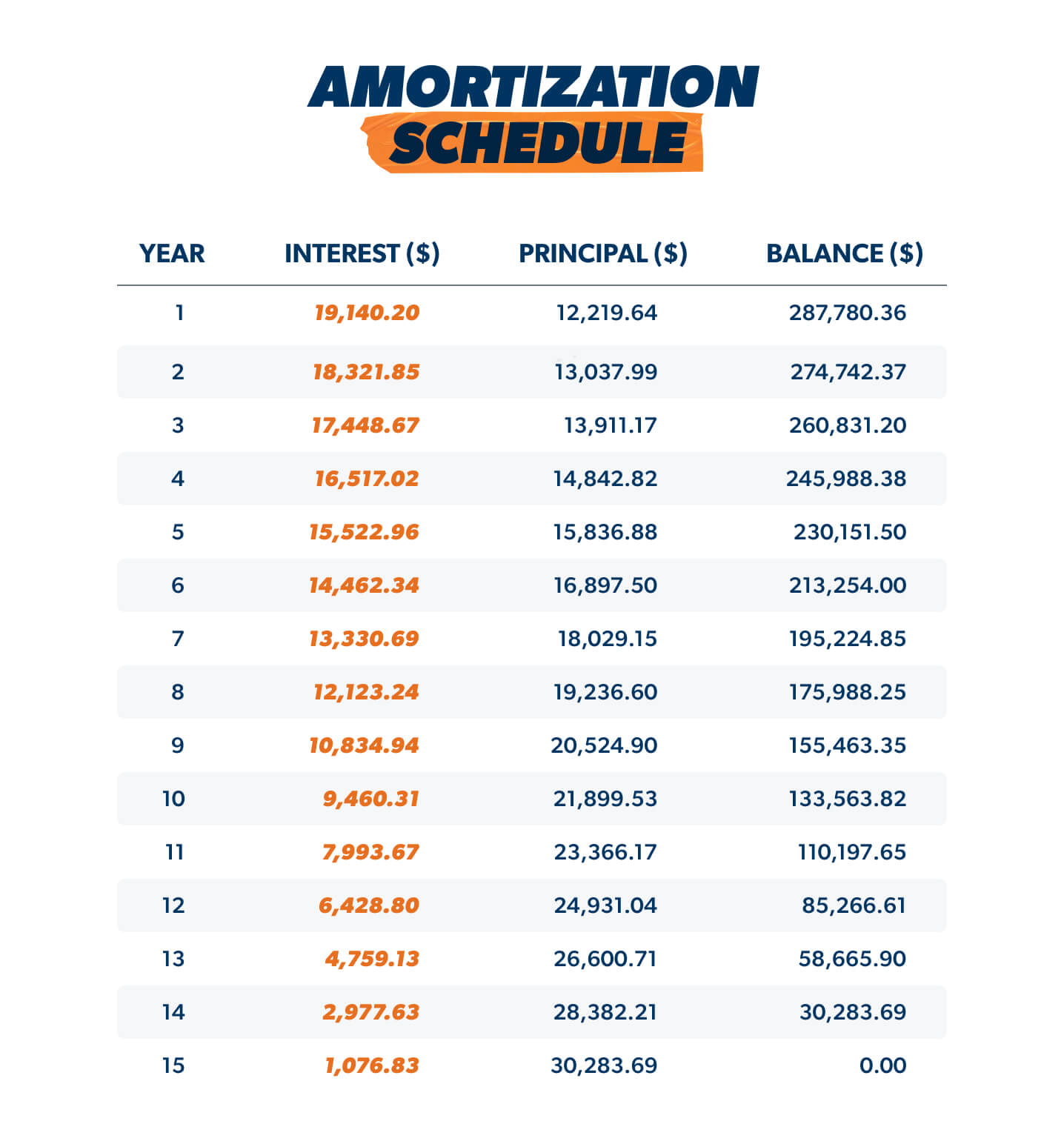

The California Mortgage Interest Deduction enables eligible homeowners to reduce their taxable income by subtracting interest paid on mortgage loans used to purchase, build, or renovate a primary residence. Unlike the federal deduction (subject to recent limits), California’s version applies to interest on loans up to a determined annual threshold—allowing homeowners to claim a portion of their interest expense as a tax reduction based on actual payments. Universal Studios California In One Day When Are Watermelons In Season In California

Eligibility requires the home to be used as a main dwelling unit and interest must be on a qualified loan. The process begins with accurate record-keeping of mortgage payments, and tax filers report on standard Schedule A. While the deduction does not guarantee full tax savings, it can significantly lower overall liability during high-interest cycles, especially when combined with other deductions like property taxes.

Common Questions About the California Mortgage Interest Deduction

H3: Do homeowners owe state taxes in addition to federal? Yes—California residents report mortgage interest on federal tax returns via Schedule A but also file state taxes separately, where interest may be treated differently. Homeowners should factor in both systems when planning deductions.

H3: What if I only partially qualify? The deduction is prorated based on qualifying interest paid. Restoring Gun Rights In California Poor record-keeping may reduce claimable amounts, so accurate documentation is essential.

H3: Can this deduction apply to refinanced loans? Yes—refinancing that maintains or increases mortgage interest qualifies, but only the interest portion post-approval counts toward the annual deduction limit.

H3: Does this deduction impact eligibility for other homeowner credits? It may influence adjusted gross income but does not disqualify eligibility for credits—each is assessed independently.

Opportunities and Considerations

Pros: Offsets rising home interest costs Supports long-term savings in high-cost markets Can reduce federal taxable income meaningfully

Cons: Eligibility limits apply annually Subject to IRS and state compliance rules Benefits vary by income and loan type

For many, the deduction offers practical tax relief but requires understanding annual caps and documentation expectations. Realizing its value means planning ahead and consulting updated IRS and state guidelines.

Misconceptions About the Deduction

One widespread myth is that it applies tax-on-tax—this is false. The deduction directly reduces the amount of interest income reported for tax purposes, not total tax owed. Another misconception is that it applies to all homeownership costs—only interest on qualified mortgage debt qualifies, excluding property taxes or fees unless tied to interest.

Clarifying these points builds trust and ensures accurate use. The deduction is a useful tool, not a universal homeownership shortcut.

Who Should Consider the California Mortgage Interest Deduction?

1. First-time homebuyers seeking tools to lower ongoing costs 2. Existing homeowners refinancing or renovating, aiming to keep finances optimized 3. Investors managing property portfolios with interest-heavy loans 4. Low-to-moderate income families aiming to reduce annual tax liabilities

The benefit is most meaningful in years with high mortgage balances and sustained interest payments—making it a relevant consideration when evaluating ownership costs.

Encourage Exploration Without Promotion

Understanding the California Mortgage Interest Deduction is key to smarter financial planning—especially during periods of shifting tax and housing markets. While it may ease month-to-month expenses, realistic expectations about timing and limits help homeowners make informed choices. Exploring this deduction as part of a broader tax strategy supports long-term stability, not quick fixes.

Stay informed, review current limits each year, and consider consulting a tax professional to maximize benefits legally and accurately. With attention to detail and consistent planning, this lesser-known advantage can quietly strengthen financial well-being across the state.