Understanding Hardship License California: A Growing Conversation in the US

Why are so many users now exploring Hardship License California during a time of rising financial stress and housing uncertainty? This streamlined license offers a critical path for homeowners facing economic hardship, providing a legal framework to reduce burdens on mortgages when hardship strikes. With California’s tight housing market and soaring costs, this solution is gaining traction nationwide—not as a quick fix, but as a thoughtful mechanism designed to support those struggling to keep pace. Pizza Palace California Style Menu

Why Hardship License California Is Gaining Attention in the US

In recent years, increasing financial strain across the country has intensified public discourse around housing stability and debt relief. Within this context, Hardship License California has emerged as a key topic among users searching for reliable, localized support during tough times. Media coverage, financial literacy platforms, and homeownership advocacy groups are highlighting how this license allows eligible homeowners to pause or reduce mortgage payments under verified hardship—without foreclosure. California Weather In Fall The mix of rising housing costs, limited affordable options, and growing awareness of consumer protections fuels organic interest, positioning the license as more than a legal formality, but as a vital tool for financial resilience.

How Hardship License California Actually Works

The Hardship License California is a state-designated legal request that lets homeowners temporarily suspend or reduce mortgage payments when facing genuine financial distress. Pizza Palace California Style Menu To qualify, individuals must demonstrate a bona fide inability to meet payment obligations, verified through financial documentation and local housing authority review. California Legislative Process The process involves submitting proof of income loss, medical emergencies, or other qualifying hardships, followed by a assessment that balances creditor interests with borrower protection. Unlike foreclosure, this option provides a structured, supervised path forward—designed to prevent crisis while respecting legal obligations. It’s not automatic; it requires engaged verification but offers a lifeline where traditional foreclosure looms.

Common Questions People Have About Hardship License California

Q: Is this license only for people in foreclosure? Pizza Palace California Style Menu A: No—this option supports homeowners facing documented hardship regardless of foreclosure eligibility. It’s available even if payments haven’t missed yet but a financial shock is imminent.

Q: How long does the Hardship License last? A: Typically, the license spans 6 to 12 months, extendable only under redefined hardship and approved by authorities. There’s no guaranteed indefinite relief, only a structured window for repayment adjustments.

Q: Does it affect credit scores? A: Widespread credit reporting is limited—most records remain confidential during the process. However, late payments outside the program may still impact credit, so careful handling is essential.

Q: Who qualifies? A: Qualification depends on verifiable financial documentation—including proof of income disruption, medical costs, or documented emergencies—along with local housing authority approval.

Opportunities and Considerations

The Hardship License California presents meaningful opportunities for those navigating unexpected financial strain. For homeowners, it offers a regulated alternative to foreclosure, allowing time to stabilize income or seek assistance while curbing debt pressure. From a lender perspective, it balances risk exposure with consumer responsibility and regulatory compliance. Still, it’s not a universal solution—reusquirement documentation is crucial, and success hinges on honest, timely application. Understanding these dynamics helps set realistic expectations and fosters trust in the process.

Misconceptions About Hardship License California

A frequent myth is that this license guarantees immediate debt elimination—often not accurate. It only temporarily eases obligations; long-term stability requires proactive financial planning. Some believe the process is fast and automatic, but thorough review and local authority involvement are standard. Others think only foreclosure applicers qualify, when in fact it’s available proactively. With edge cases carefully managed through verification, this tool remains ethically grounded and legally supported, designed to protect both borrowers and lenders.

Who Hardship License California May Be Relevant For

Beyond homeowners facing foreclosure, this option matters for renters in rapidly devaluing markets or self-employed individuals dealing with irregular income. Small business owners under financial stress might also explore it when property obligations threaten liquidity. Each case requires a personalized evaluation—especially income fluctuations or unexpected expenses—ensuring the license serves as a strategic, not generic, resource.

A Thoughtful CTA: Stay Informed, Stay Empowered

Rising economic uncertainties highlight the importance of informed decisions. The Hardship License California is more than a legal formality—it’s a genuine support option for those navigating financial hardship in an unpredictable landscape. While outcomes vary, understanding its purpose, process, and boundaries empowers users to explore this tool with clarity and confidence. Stay informed, consult local experts, and prioritize transparency—this step toward financial resilience begins with knowledge, not pressure.

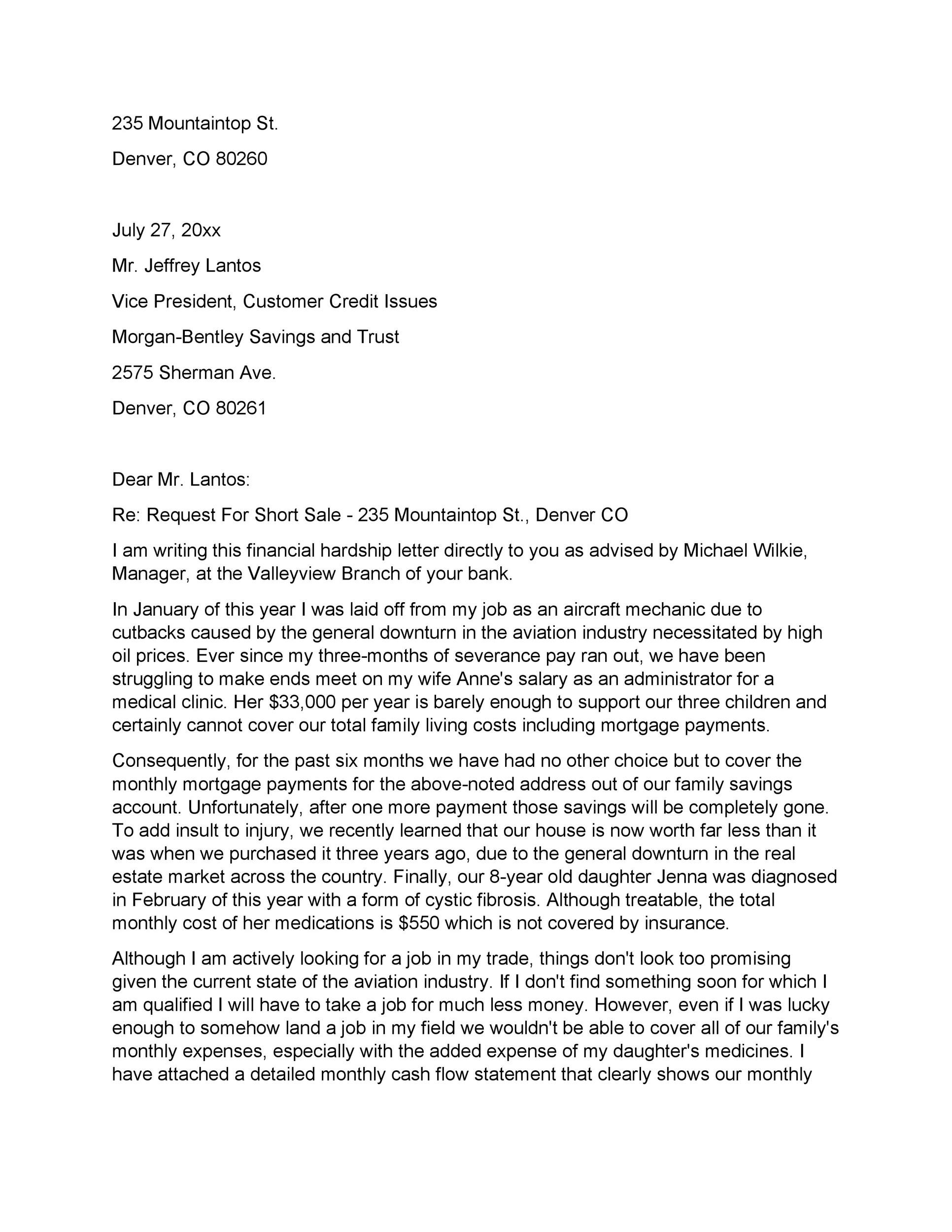

![Free Printable Hardship Letter Example [PDF, Word] Financial & Immigration](https://www.typecalendar.com/wp-content/uploads/2023/05/letter-of-hardship-example.jpg)