How Does Gap Insurance Work in California: A Clear Guide for Informed Decisions

Curious about how Gap Insurance shapes coverage for California residents—or why more Californians are exploring it now? Understanding how Gap Insurance works in the Golden State starts with recognizing how modern auto owners balance affordability, coverage, and regional needs. As trends in insurance evolve, Gap Insurance has emerged as a relevant option for navigating complex needs—especially where employer-provided policies fall short. How Long Do Evictions Stay On Your Record In California

Why Gap Insurance Is Gaining Attention in the US The growing demand for flexible, supplemental auto protection reflects changing economic realities. Many California drivers face high premiums and rising repair costs, especially in a state known for dense traffic, claim-rich zones, and specific regulatory demands. Gap Insurance addresses these gaps by bridging coverage between primary policies and real-world needs—particularly when leaving a vehicle damaged or repossessed. As DIY insurance comparisons increase online, Gap’s structured approach resonates with users seeking clarity without complexity.

How Gap Insurance Actually Works in California

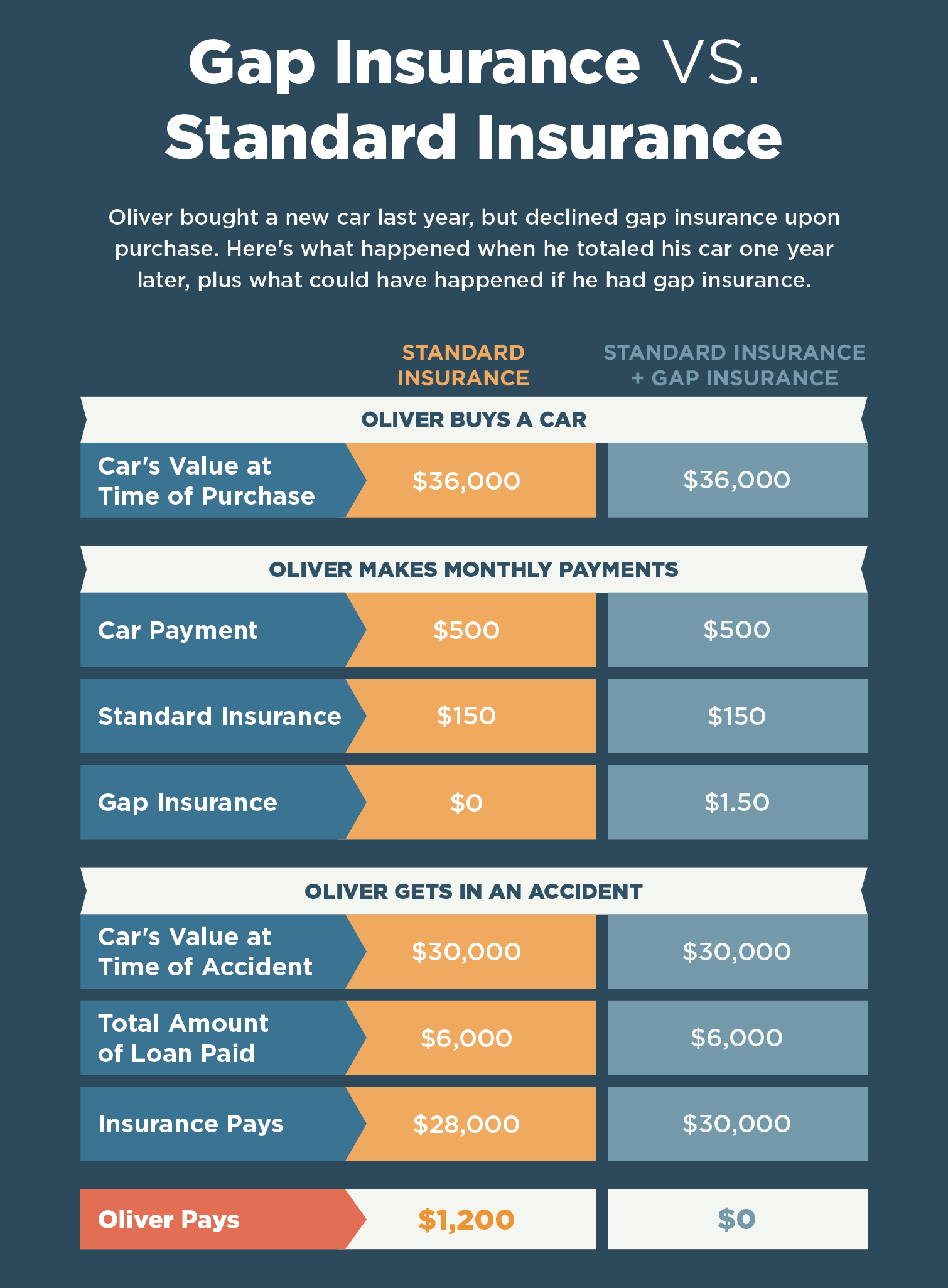

Gap Insurance protects the difference between what your vehicle’s actual cash value (ACV) and the remaining loan or lease balance is. How Long Do Evictions Stay On Your Record In California If your car is totaled or stolen, the policy covers the shortfall after your existing coverage. This is crucial in California, where vehicle values tend to be high and liability exposure is elevated.

Unlike basic collision coverage, Gap Insurance activates only when full liability payouts fall short of your loan owed. It’s often recommended after refinancing, trade-ins, or when owning high-value cars such as luxury models or electric vehicles—common among California’s diverse driving population. The policy does not replace primary auto insurance but complements it as a financial safeguard. Dove Hunting California How Long Do Evictions Stay On Your Record In California

In California, Gap Insurance is governed by state requirements, particularly for leased or financed vehicles. Lenders often mandate this coverage, but consumers increasingly turn to Gap Insurance as a streamlined solution. The process is simple: during claims filing, the insurer assesses the ACV, matches the loan balance, and covers any remaining deficit. This reduces out-of-pocket strain during recovery.

Common Questions About How Gap Insurance Works in California

Q: How much does Gap Insurance cost in California? Rates depend on vehicle age, coverage level, credit history, and creditworthiness. Many drivers see modest premiums relative to total auto costs, especially when paired with standard policies.

Q: Do I need a separate policy? No. Gap Insurance works alongside your existing auto insurance, applying only when coverage gaps emerge. Best Place To Jet Ski In California It’s not a standalone plan but a targeted financial buffer.

Q: Can I purchase Gap Insurance directly from my lender or a broker? Yes. Most banks, dealerships, or third-party carriers offer it at the point of sale, often with streamlined documentation requiring proof of ownership and valuation. Mobile-optimized portals simplify initial enrollment.

Q: Does California regulate Gap Insurance? Yes. State law mandates fair valuation practices, clear disclosure, and transparency in claims handling—protecting consumers from misrepresentation.

Opportunities and Realistic Considerations

Pros: - Covers costly gaps not fully protected by standard liability or collision policies - Designed for specific financial situations, like repossession or total loss - Quick claims processing when ACV and loan balances align clearly

Cons: - Requires proof of vehicle value and loan details upfront - Limited to vehicles used under a financing or leasing agreement - Premiums depend on credit and loan history—higher for those with limited financial profiles

Misunderstandings and Misconceptions

Many assume Gap Insurance covers daily driving expenses or comprehensive theft—not true. It activates strictly during total loss when full settlement gaps exist. Others believe it replaces full coverage, but it must be paired with primary insurance. These distinctions ensure users avoid overestimating benefits and make informed choices.

Who Might Find Gap Insurance Relevant in California

- New car buyers financing vehicles through leases or loans - Used car owners upgrading or replacing older models - Urban drivers facing high repair costs in California’s congested markets - Lemon or high-end vehicle owners needing tailored protection beyond lender mandates

Soft CTA: Stay Informed, Compare Wisely

Understanding how Gap Insurance works in California empowers smarter decisions at a critical time when insurance complexity grows. While it’s not a universal fix, it serves a clear role in mitigating financial risk—especially when paired with routine vehicle maintenance and policy review. Take control of your coverage by learning how Gap fits your situation. Explore options, assess your loan terms, and ensure your assets stay protected—without sacrificing clarity or control.

The landscape of insurance in California evolves fast, and staying informed is the best shield. Let curiosity guide your next step.