Discover the Growing Movement Around Roth Ira California – Guidance for Informed Choices

Why are more U.S. residents turning to Roth Ira California as a key financial tool in a shifting retirement landscape? With rising costs of living, increasing awareness of tax-advantaged savings, and California’s unique demographic and economic dynamics, this California-specific IRA option is quietly gaining momentum. Train From Seattle To San Jose California It offers a tailored path to max out contributions, reduce taxable income, and build retirement security—without the complexity of traditional plans. As more individuals seek smart, personalized retirement strategies, Roth Ira California is emerging as a relevant choice for savvy savers across the state.

Why Roth Ira California Is Gaining Attention in the U.S.

Today’s uncertainty around retirement savings—slow employer plans, shifting Social Security projections, and rising healthcare expenses—has sparked renewed interest in effective, state-optimized tools. Roth Ira California stands out by blending federal flexibility with California-specific benefits, especially for residents navigating tight tax brackets and high living costs. Train From Seattle To San Jose California Its growing mention across personal finance forums, digital newsletters, and financial literacy campaigns reflects a rising awareness: this is more than a local IRA—it’s a strategic retirement solution in demand.

Mobile users exploring retirement plans often find Roth Ira California through concise, insight-driven search results, drawn by clarity and practical value. With easy qualification, no income phase-outs for certain earners, and state-level rebates or incentives, it appeals to both new and experienced savers seeking simplicity and growth. As digital discovery grows, so does understanding of how Roth Ira California supports long-term financial resilience.

How Roth Ira California Actually Works

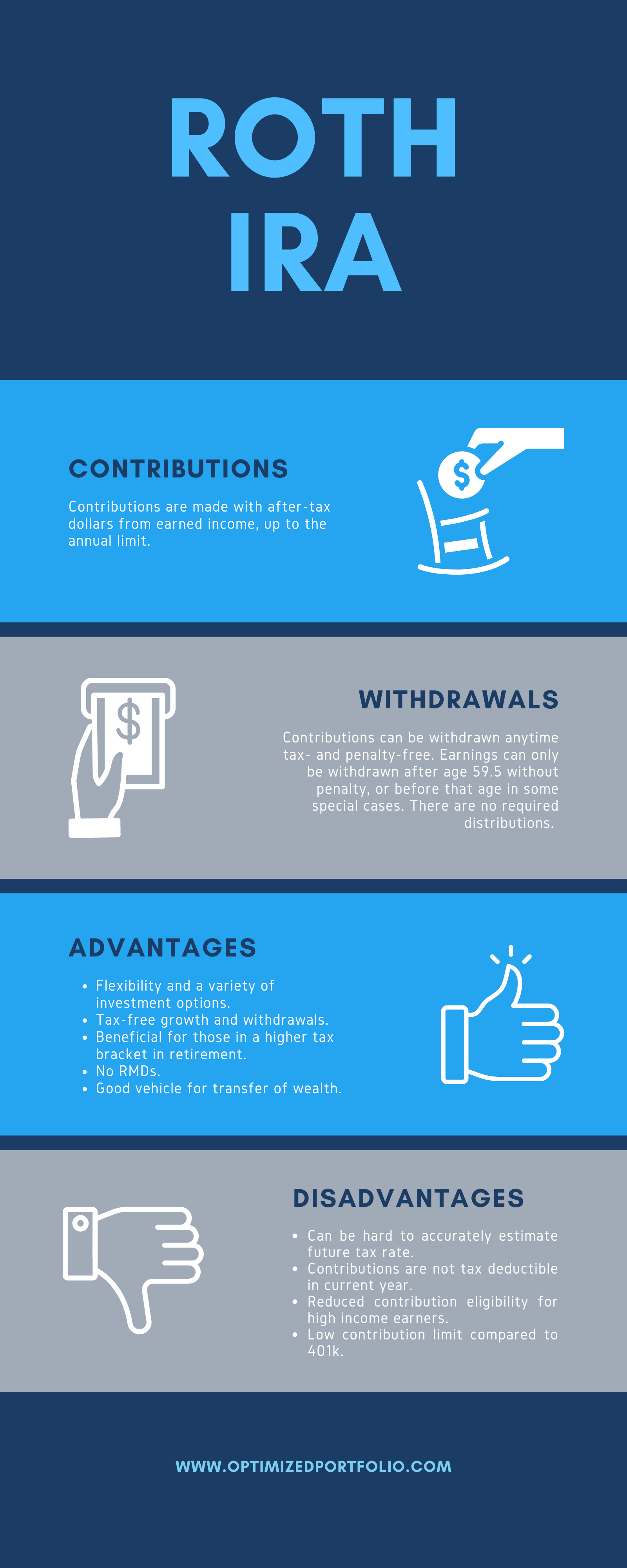

Roth Ira California is an IRA account available to California residents that combines the federal Roth IRA structure with state-adapted rules. Train From Seattle To San Jose California It allows qualified contributions each year based on income eligibility—often no phase-outs for middle- and lower-income earners, making it accessible to a broad audience. Contributions grow tax-free, and qualified withdrawals in retirement are completely tax-free, offering powerful long-term savings. Unlike traditional IRAs, no required minimum distributions early on, giving flexibility in planning.

Specifically, California residents benefit from local tax incentives and streamlined administration, reducing friction when opening and managing the account. The process is digital-first: apply online, fund the account via banking links, update contributions annually—all optimized for mobile use. This modern setup encourages engagement without jargon, keeping users informed and in control.

Common Questions About Roth Ira California

What’s the income limit to open a Roth Ira California? For 2024, those earning under $145,000 annually qualify for full contributions without phase-outs, making it accessible to middle-income Californians. Higher earners retain partial benefits through income-adjusted eligibility, preserving access for many.

Can Roth Ira California be used alongside other retirement accounts? Yes. It fits within overall tax planning alongside 401(k)s and traditional IRAs, allowing users to layer retirement savings while meeting personal income limits and tax goals.

Does Roth Ira California offer state tax benefits? Peonies In Southern California While federal, its structure aligns with California’s progressive tax environment, encouraging long-term savings and reducing taxable income annually— advantageous in a high-tax state.

What kind of investments can I hold? Users enjoy full control over tax-free growth with access to bonds, mutual funds, ETFs, and stocks—consistent with standard Roth IRA options, but with California’s financial ecosystem influence. California Drift Events

Opportunities and Considerations

Roth Ira California offers significant upside: tax-free compound growth, potential state-side incentives, and role as a foundational retirement layer. It suits candidates who value long-term planning, want to lower current tax burdens, and prefer flexible, transparent savings.

But users should recognize limitations—contribution caps and income rules apply, and results depend on investment choices and market conditions. It’s not a guaranteed income replacement, but a disciplined path toward financial confidence.

Things People Often Misunderstand

Myth: Only high earners benefit. Reality: Most eligible Californians—especially those in mid-income brackets—find Roth Ira California immediately accessible and valuable.

Myth: Contributions are tied to employer plans. Reality: It’s an individual account, open to self-employed, independent contractors, and traditional employees alike.

Myth: All IRA types offer the same tax treatment. Reality: Roth Ira California’s structure balances tax deferral benefits with user-friendly California-focused rules, distinguishing it from other state-agnostic IRAs.

Who Roth Ira California May Be Relevant For

Budget-conscious Californians building retirement wealth without employer match dependence, young professionals planning career shifts, small business owners consolidating savings, and immigrants or non-U.S. citizens seeking U.S. retirement foundations—this account serves diverse life stages and financial situations.

associent of personal finance neutral and informative, these insights empower users to explore Roth Ira California as a flexible, responsible tool—not a quick fix. With clarity, context, and alignment to real-life goals, it supports smarter financial decisions, reflecting real demand trending across mobile-first U.S. users.

Soft CTA

Discover more about how Roth Ira California fits your retirement vision—not with pressure, but with clarity. Take a moment to explore your eligibility, review contribution limits, and see how this IRA could support your long-term security. Staying informed is the strongest step toward financial confidence.